Effective 22nd June 2009, Lagos State Government has imposed a 5% consumption tax on all purchases of goods and services sold to consumers in any restaurant, hotel, event center and entertainment venue (bars, clubs, lounges).

The owner of the restaurant, hotel, event centre, etc is obligated to register with the Lagos State Internal Revenue Service (LIRS) as a collecting agent. The collecting agent must charge and collect 5% consumption tax on all consumables and personal services and remit to the LIRS monthly.

The owners of Infinity Gold Homes are registered with the LIRS as a collecting agent and must charge 5% consumption tax. All customers of the services provided by Infinity Gold Homes. are obligated to pay the 5% consumption tax.

You’ll find copies of the LIRS Public Notice from March 2021 on Consumption Tax and the Hotel Occupancy and Restaurant Consumption Law in PDFs right / below.

VALUE ADDED TAX

Value Added Tax is a consumption tax on goods and services. The current rate of Value Added Tax (VAT) in Nigeria is 7.5%. The Federal Inland Revenue Service (FIRS) is the agency of the Federal Government that administers VAT.

Infinity Gold Homes is registered with the Federal Inland Revenue Service. Infinity Gold Homes must charge 7.5% VAT on services rendered to customers. The VAT is remitted monthly to the FIRS.

Section 2 (b) (i) and (ii) of the VAT Act states:

“(b) in respect of a service –

(i) the service is rendered in Nigeria by a person physically present in Nigeria at the time of providing the service

(ii) the service is provided to and consumed by a person in Nigeria, regardless of whether the service is rendered within or outside Nigeria or whether or not the legal or contractual obligation to render such service rests on person within or outside Nigeria.”

Section 2A (1) states:

(1) “For the purposes of this Act, supply shall be deemed to take place at the time an invoice or receipt is issued by the supplier, or payment of consideration is due to, or received by the supplier in respect of that supply, whichever occurs first.

This means that Infinity Gold Homes. must charge VAT on all supply of goods and services except those specifically listed as exempt in the VAT Act.

Any customer who requires evidence of the remittance of the VAT paid over to Infinity Gold Homes. can make a request. Our Tax Consultant will liaise with the customer and make the relevant evidence and documents available.

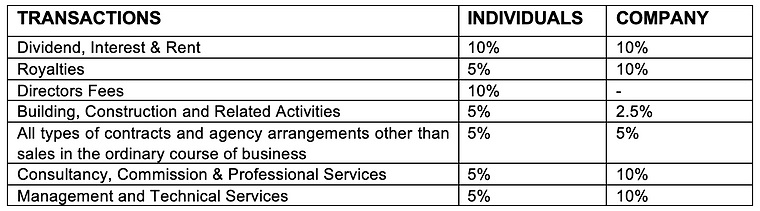

WITHHOLDING TAX

Withholding Tax is an advance payment of income tax. It is payment on account of the total income tax liability of the taxpayer. WHT is normally deducted at source when payment is made. The payer (acting as an agent to the relevant tax authority) is empowered by law to effect WHT deduction, and thereafter, pay to the beneficiary an amount less than the withholding tax deducted from the gross amount.